After the dust has settled: Optics and Reality Check of Trump’s Gulf trip

US President Donald J. Trump’s visit to Saudi Arabia, the United Arab Emirates (UAE), and Qatar from 13-15 May 2025 drew significant attention and was broadly assessed as a strategic success from both US and Gulf perspectives. The trip was marked by the announcement of high-value trade and investment agreements and framed by a notably warm reception from Gulf leaders. Therefore, the trip demonstrated renewed commitment to long-term strategic partnership in investment and artificial intelligence (AI) as well as regarding tariffs and strong personal ties.

Despite the optimistic tone and the positive optics, though, substantive challenges exist as Gulf states need to pursue a careful balancing act: On the one hand, they have to leverage close ties to Trump while on the other hand advancing domestic economic diversification and managing geopolitical polarization in light of declining oil revenues and global trade frictions. This includes maintaining strong commercial relations with China and other US competitors which reflects the Gulf states’ omni-balancing strategy rooted in pragmatism.

For European policymakers, the visit provides a critical inflection point to reassess their engagement strategies with both the Gulf and a second Trump administration.

The investment dimension

Accompanied by various CEO of the US business community, Trump presented himself as a businessman and dealmaker to push for economic partnerships and defense cooperation during his trip to Riyadh, Abu Dhabi, and Qatar. In general, the White House announced more than 2 trillion USD in trade and investment deals with Saudi Arabia, the UAE, and Qatar. Trump has highlighted this result as a significant success to boost his transactional MAGA agenda. Additionally, Gulf officials further underlined the strategic relevance of the economic partnership making them a win-win situation.

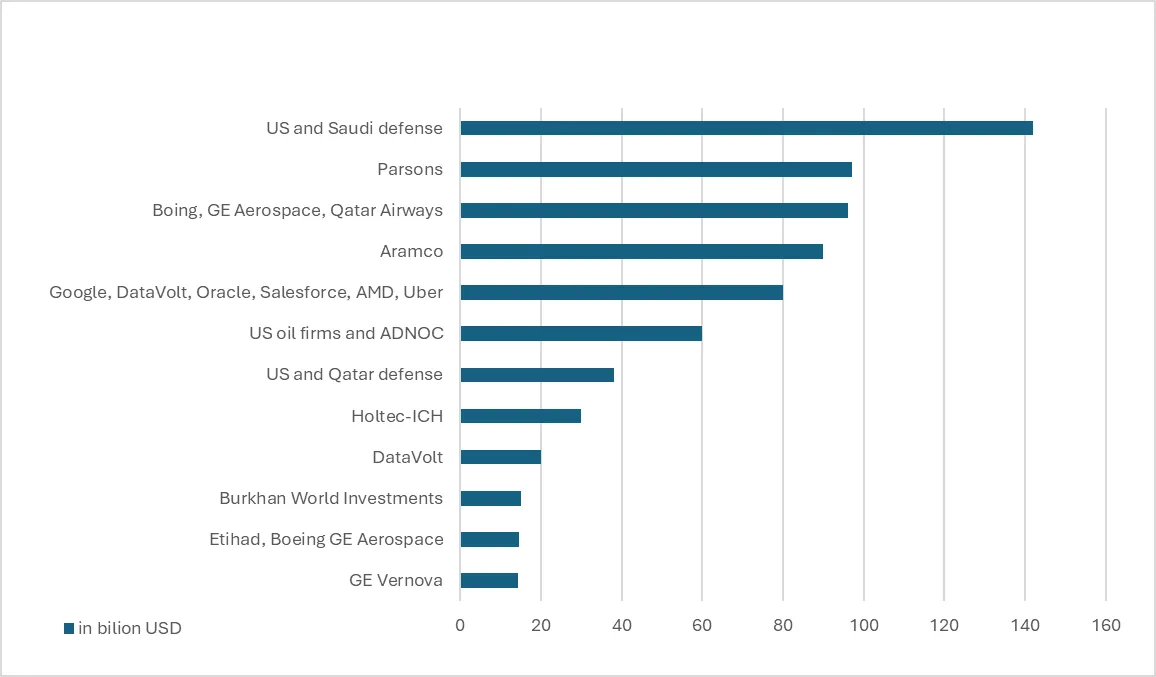

- Saudi Arabia: In Riyadh, a series of business deals covering defense, energy, space, and air transport were released: Totaling USD 600 billion, Saudi Arabia announced to invest into the US over the next four years. As part of this package, military contracts worth of USD 142 billion were signed with more than ten US defense contractors. Additionally, Saudi Arabia finalized agreements totaling USD 14.2 billion for gas turbines and related energy technologies, along with a separate USD 4.8 billion procurement of Boeing commercial aircraft. The kingdom’s oil giant Saudi Aramco signed 34 agreements with US companies, potentially worth up to USD 90 billion across AI infrastructure and other sectors. In concrete terms, Aramco plans to expand the Motiva refinery in Texas by investing USD 3.4 billion. US construction firms such as Hill International, Jacobs, Parsons, and AECOM are further engaged in several infrastructure projects such as the King Salman International Airport, King Salman Park and Qiddiya City with more than USD 2 billion. Furthermore, the agreements encompassed a broad spectrum of strategic cooperation, including a letter of intent focused on future defense capabilities, a MoU with the US Department of Justice, and collaborative frameworks addressing space exploration and infectious disease research. Notably, the package featured an agreement between NASA and the Saudi Space Agency to deploy a Saudi-developed CubeSat aboard NASA’s Artemis II mission. This satellite will monitor space weather conditions across varying distances from Earth, marking a significant milestone in bilateral space collaboration.

- The UAE: In the UAE, the Emirati and the US governments stated to sign deals worth USD 1.4 trillion including investments in AI, cloud-computing infrastructure, semiconductors, energy, and manufacturing. Highlights include a USD 14.5 billion aircraft deal between Etihad Airways, Boeing, and GE Aerospace, a USD 4 billion aluminum smelter investment in Oklahoma, and a USD 60 billion energy partnership involving ADNOC and leading US firms.

- Qatar: In the Qatari case, the most prominent deal was in aviation: Boeing and GE Aerospace secured a landmark USD 96 billion deal with Qatar Airways for the acquisition of up to 210 US-manufactured Boeing 787 Dreamliner and 777X aircraft, powered by GE Aerospace engines. In the military sector, Qatar aims to invest USD 10 billion to upgrade US military facilities located in the country such as the Al Udaid US military base. Here, General Atomics finalized a nearly USD 2 billion deal for the sale of the MQ-9B remotely piloted aircraft system to Qatar. In the energy sector, McDermott is currently executing seven active projects valued at USD 8.5 billion with Qatar Energy. In engineering and infrastructure development, Parsons is involved in 30 projects with an estimated value of USD 97 billion.

Despite such expressive numbers, the substance of such announcements has to be put in question: In contrast to the officially mentioned USD 2 trillion in combined deals, Reuters calculated the total value was just USD 700 billion. Most of such deals were announced weeks or months before the Trump trip and numbers are varying: The White House fact sheet just mentions USD 283 billion in Saudi investments which is only half of the original amount of USD 600 billion. In terms of the Aramco investment package, the majority of these agreements were non-binding memoranda of understanding (MoU), with many lacking specified monetary values.

Experts estimate that the proposed USD 600 billion investment package (averaging USD 150 billion annually over four years) would represent roughly 14% of Saudi Arabia’s GDP, 40% of its export revenues, and more than half of its annual import bill. Yet, current trade patterns show the US accounts for only 9% of Saudi goods imports in 2024, compared to 23% from China. Even under optimistic projections of 10% annual growth, total US exports to Saudi Arabia during a four-year Trump presidency would reach just USD 125 billion in total. As a result, the remaining USD 475 billion of the USD 600 billion commitment would thus need to be fulfilled through new Saudi investments in the US.

These figures suggest that the scale of the commitment may pose significant implementation challenges and is too ambitious. In particular in times of low oil prices and ongoing regional crises, the Saudi economy will suffer from decreasing revenues and face current account deficits from 2025 to 2028 which will also impact its resources for foreign investment. Without these surpluses, any additional investments in the US would need to come from reallocating existing foreign assets or raising capital through debt or asset sales and requires to putting potentially over 80% of all Saudi foreign assets in the US.

In the Qatari case, a similar significant discrepancy exists: An ‘economic exchange’ valued at a minimum of USD 1.2 trillion was announced during Trump’s visit to Qatar. However, the official White House fact sheet outlined confirmed agreements totaling only USD 243.5 billion between the US and Qatar.

Neither Trump nor his Gulf counterparts appear concerned with such opaque or potentially inflated nature of the investment figures announced. From their perspective, the symbolic value of these commitments outweighs the need for immediate financial verification, as the announcements serve broader strategic and political objectives rather than purely commercial benchmarks. The significance of these deals lies less in whether every announced amount is backed by concrete commercial activity, but more in the strategic message they convey: the Gulf states are not merely financial backers for the US, but are being positioned as preferred political partners in a shifting global landscape. Against this backdrop, they consider such ambitious announcements as symbolic dividends.

Notwithstanding, it will remain a challenge for some Gulf states to balance its commitments for investment in the US as they need to preserve domestic returns. Saudi Arabia stands out as a key case study in the region, with a strong emphasis on domestic investment in large-scale infrastructure, urban development, tourism, and entertainment. These efforts aim to address pressing socio-economic needs such as affordable housing, public transportation, and educational facilities while simultaneously positioning the kingdom to host major international events, including the 2029 Asian Winter Games, the 2030 Riyadh Expo, and the 2034 FIFA World Cup. To meet these ambitious goals, Saudi Arabia must secure substantial foreign direct investment (FDI) as a critical pillar of its economic transformation strategy.

However, FDI declined for the third consecutive year in 2024. As the kingdom needs a breakeven oil price ranging between USD 95 and USD 113 per barrel to balance its budget, it has to reduce government spending in times of lower oil prices which could further hamper its ambitious domestic diversification plans. In light of such necessities and amid times of declining state finances, Saudi Arabia has to strike a balancing act between strongly required domestic investments and other business activities in external markets such as the US. Whereas the Saudi government is seeking stronger commitment from US multinational firms and investors, Trump is considering Saudi partners as ‘ATM’s’ to boost investments inside the US – a dilemma that could result in frictions in the US-Saudi relations.

The tariff dimension

So far, the high tariffs introduced by Trump do not necessarily affect the Gulf states directly as all of them are just facing tariff rates of 10% – much lower than other markets in Europe or Asia. Since oil, gas, and refined products will be exempt from the new tariffs, the direct impacts are expected to be limited.

Nevertheless, indirect consequences of a global tariff war will also impact Gulf economies in terms of higher export costs, potential trade diversion, and energy market volatility. US-caused economic unpredictability may keep oil prices low which could reduce demand from Gulf states’ main customers in Asia such as China. As a consequence, the imposition of tariffs could spur a global economic recession which would also undermine the economic aspirations of the Gulf states. Here, Trump’s zigzag actions regarding tariff restrictions are also considered in the Gulf as an element of uncertainty for the stability of the global economy. Accordingly, higher tariffs on steel and aluminium could strain the industrial sectors of the UAE and Bahrain. The UAE, notably, is the second-largest aluminium exporter to the US. Additionally, the more US tariffs are disrupting China’s economy, the more Gulf states will face the implications as Beijing has become the most relevant trade partners for most of them.

The AI dimension

Both the Gulf states and the US are strengthening their cooperation in AI. Gulf leaders are seeking privileged access to advanced US semiconductor technology as such technology remains subject to strict export controls for most countries. In particular, the UAE positions itself as a tech and AI powerhouse in the region as several agreements were signed prior to and during Trump’s trip to the Emirates: Already in March, new commitments from NVIDIA and xAI as part of the AI Infrastructure Partnership were announced. In the UAE, US cloud and data companies have intensified their engagement: Microsoft opened new hyperscale data centers in Abu Dhabi and Dubai, Amazon Web Services has launched its Middle East (UAE) Region branch in the Emirates, and other US tech companies are enhancing joint ventures, capacity development and training programs in the UAE with local partners. Mubadala has already invested in US tech and AI companies such as AMD, GlobalFoundries, and Waymo and has started to cooperate with tech startups, especially in AI, fintech, and health-tech located in Silicon Valley. Additional agreements comprise of a USD 20 billion investment in US data centers such as a USD 335 investment of Abu Dhabi-based G42 US chip startup Cerebras.

In contrast to the UAE, Saudi Arabia has just started recently to strategically invest into the AI industry. However, the kingdom follows ambitious plans to position itself as a regional digital and tech hub for compute infrastructure by launching its new state-own AI company HumAIn shortly before Trump trip to Riyadh. The company aims to develop 1.9 gigawatt (GW) of data center capacity by 2030, expanding to 6.6 GW by 2034 with total costs of USD 77 billion. During Trump’s visit, it was announced that HumAIn entered a partnership agreement with the US technology giant Qualcomm. Both companies intend to cooperate in the fields of AI data centers development and semiconductor production. Additional HumAIn partnerships comprise of plans to construct AI factories with NVIDIA, entering a joint venture with AMD to jointly invest USD 100 billion in a 500 MW data center, and cooperating with Amazon Web Services to develop a USD-5-billion special cluster of data centers on Saudi soil. Additionally, the Saudi data center company DataVolt signed a multi-year agreement with US server company Super Micro Computer Inc. (Supermicro).

Investing in digital infrastructure does not only aim to strengthening partnerships with US tech companies but also to attracting foreign investments into the Saudi market. Here, the Saudi Public Investment Fund (PIF), chaired by Muhammad bin Salman, serves as the main driver of investments by allocating more than USD 40 billion into AI-companies such as HumAIn among others, data centers, and semiconductors.

In Qatar, Quantinuum entered into a JV with Al Rabban Capital, under which Qatar will invest up to USD 1 billion in quantum computing technologies and workforce development.

The focus on AI fits perfectly into the Gulf digital transformation as they aim to position themselves as technological forerunners in tech-focused trendsetting aiming at consolidating their image as modern and tech-savvy digital nations, future-oriented tech champions, and drivers of technological innovation.

By signing partnerships with US tech companies, they not only aim to get better access to the US digital market but also improve the bilateral interconnections through AI diplomacy. Thus, AI investments are emerging as a strategic cornerstone of the Gulf’s diversification strategy in order to preserve political agency, technological leverage, economic sovereignty, digital modernization, and techno-industrial statecraft.

However, the Gulf states’ growing engagement in the AI industry could also draw them more directly into the spotlight of US-China strategic competition. The Gulf countries seek to deepen cooperation with both powers and are determined to avoid being pressured into choosing sides.

In seeking to maintain their strategic positioning as a swing region between the US and China, Gulf states may come under increased pressure from the Trump administration to reduce their engagement with China in favor of a closer partnership with the US. Such a scenario would counter the Gulf states’ omni-balancing strategy aimed at diversifying their geoeconomic partnerships.

Overview of the most relevant US-Gulf business agreements

Source: Reuters.

The bromance dimension

All Gulf leaders – particularly Saudi Crown Prince Mohammad bin Salman, UAE President Mohammad bin Zayed, and Qatar’s Emir Tamim bin Hamad Al Thani – have become adept at navigating Donald Trump’s distinctive approach to his transactional and personal policymaking. Characterized by deliberate disruption, and the management of uncertainty to secure advantageous outcomes, this approach creates unpredictability in negotiations. From the perspective of Gulf states, however, such transactional dynamics can also present opportunities to increase their strategic leverage in bilateral engagements.

During the first Trump administration, the Gulf governments have become aware of Trump’s policy of shaking things up which caused frustration on the Saudi and Emirati side when the Trump administration did not support their blockade against Qatar and did not provide substantial military protection for Saudi Arabia after the drone and missile attacks on two Saudi oil refineries in September 2019.

Since then, all leaders have learned their lesson and find themselves today in a better position to deal with Trump’s erratic policy style: By offering him a spectacular reception and meeting his expectations in terms of business deals, they further strengthen mutual trust and cultivate the image of ‘bromances’. Similar to Trump, Gulf leaders also present themselves as powerful leaders who aim to change their societies in drastic ways by marginalizing old influential elites.

Qatar’s Emir Tamim, for instance, actively promoted close ties with Trump after he was pushed by Abu Dhabi and Riyadh during his first term to exert more pressure on Doha. As Qatar is hosting the Al Udeid base, it significantly contributes to US security which is providing additional leverage on Trump. Therefore, the partnership with the US constitutes a significant pillar of Qatar’s security indicated by expanded Qatari lobbying in Washington.

The evolving partnership is grounded in a mutual recognition of complementary strengths: Qatar leverages its financial resources and global networks to enhance its diplomatic relations with the US, while Washington contributes security guarantees, strategic access, and international legitimacy. The bilateral framework is built on two foundational elements: (1) Qatar’s function as a key economic and diplomatic actor in the region, and (2) its growing role as a significant investor in sectors critical to US strategic interests.

Furthermore, personal business interests of Trump and his family are driving the close relations with Gulf leaders: in Jeddah, Riyadh, and Dubai, the construction of Trump Towers are under negotiation, whereas the Trump International Golf Club is planned to be developed in Qatar. Since his first term, those personal business links have become an integral part of Trump-Gulf relations: He was personally involved in the negotiations about the merger of the Saudi-financed Gulf LIV Tour and the US PGA Tour. His son-in-law Jared Kushner’s private equity firm Affinity Partners received a USD 2 billion investment from PIF. Finally, it was revealed that USD1, a crypto firm linked to the Trump family, was planned to enable a transaction between the UAE’s MGX investment fund and Binance, the world’s largest cryptocurrency exchange.

Personal business interests thus play a significant role in Trump’s relations with Gulf leaders and business elites which has caused criticism regarding accountability and conflict of interests. For instance, Qatar was providing Trump a new Boing 747 airplane as a gift which was framed as ‘corruption’. For the Gulf leaders, though, such hybrid private-official way of dealmaking does not cause a huge challenge as long as the return on investments in terms of personal credibility, economic dividends, and political leverage meet their expectations.

Implications for Europe

As elements of ‘Trumpism’ may clash with Gulf priorities, particularly economic stability, the perceived honeymoon between Trump and the Gulf could weaken. In times of declining fossil resources and rapid change, all Gulf states have to navigate the complexities of economic reform, regional stability, and strategic independence. The extent to which they can move beyond binary choices and reject zero-sum thinking in favor of mutually beneficial strategies will be the key determinant in shaping future partnerships. In particular, they need to demonstrate Gulf agency towards the US in light of close ties to US rivals such as Russia and China.

From an economic perspective, some Gulf states view Trump’s isolationist and disruptive policies as potential risks to the credibility and attractiveness of the US market as a destination for Gulf investments. As the Trump visit has shown, US-Gulf ties are strong, but also reliant on Trump’s unpredictability – an issue for Gulf states. This perception could prompt a reassessment of their investment strategies, potentially leading to a gradual shift toward alternative markets, particularly in Europe. Despite the fact that Europe’s political and economic reputation has suffered in recent years, Europe still constitutes an attractive and reliable business partner for the Gulf states. As European countries seek to diversify partnership models amid ongoing transatlantic tensions and the war in Ukraine, enhanced cooperation with Gulf states presents a valuable opportunity for investment and knowledge transfer.

Against this backdrop, the European Union (EU) and the UAE have officially started negotiations for a bilateral free trade agreement (FTA). If concluded, this would represent the first comprehensive trade agreement between the EU and a country in the Gulf region. The initial negotiation rounds will focus on reducing tariffs on goods, improving market access for services, and facilitating digital trade and investment. Discussions will also address cooperation in sectors of mutual interest, such as renewable energy, green hydrogen, and critical raw materials. These talks take place in the context of ongoing economic transformation efforts in both the EU and the UAE, particularly in relation to digitalization and climate objectives. The agreement may also support broader trade and investment flows across areas including digital technologies, AI, financial services, space, advanced manufacturing, healthcare, infrastructure, logistics, and sustainable food systems. In times of global crises, this negotiation process reflects a shared interest in strengthening economic ties and exploring opportunities for expanded cooperation in sectors relevant to long-term development goals.

Nonetheless, challenges persist: From the Emirati perspective, the EU is often viewed as a bureaucratically over-bloated actor with slow and fragmented decision-making processes. Conversely, the EU must carefully weigh concerns related to digital security and data governance when engaging with the UAE on AI collaboration.

Furthermore, a bilateral FTA could undermine the future perspectives of FTA negotiations between the EU and the Gulf Cooperation Council (GCC) which started already in 2008 and did not reach an agreement yet. Despite statements by UAE officials, that a bilateral FTA would not undermine prospects for a comprehensive EU-GCC FTA, chances for a multilateral agreement could diminish further, as other Gulf states may be encouraged to follow the UAE’s lead and seek bilateral trade arrangements with the EU. Such a trend would weaken the collective bargaining position of the GCC.

Other Researches